The following describes the performance of the WCC portfolio for Q4 2010 and for the full 2010 year and describes the current positions in the portfolio.

Portfolio Performance:

During Q4 2010, the WCC portfolio returned 9.32% compared to 10.2% for the S&P500. For all of 2010, the WCC portfolio returned 35.60% compared to 12.78% for the S&P500.

Since inception (1/22/2008) the WCC portfolio has returned 103.44% compared to -4.04% for the S&P500.

The above return figures reflect the portfolio’s time weighted return compounded quarterly. This method strips out the distorting effects of cash deposits and withdrawals to create a useful comparison to indices or other money managers. The internal rate of return for the portfolio reflects a somewhat different return.

Market Thoughts:

During Q4, we saw equity markets continue to rise as economic activity appears to be picking up and concerns about a “double-dip” recession faded. Deflation concerns are lessening and bond yield are beginning to rise (from historical lows). Its now quite apparent that while unemployment remains high, blue chip corporate profits are experiencing a full-fledged recovery and many companies are in a stronger position than they were pre-recession. Record-low cost of debt capital combined with decreased labor cost structure and a focus on corporate efficiencies have increased margins. And now we’re beginning to see revenue growth. Extremely well run companies like IBM and Johnson & Johnson have been able to issue bonds with unreasonably low yields, adding low-cost leverage to their capital structures. While stocks are up, I continue to think that top-tier blue chip stocks remain reasonably priced (especially in the tech sector) with earnings yields in the 7-9%. Stocks look even more attractive when compared to treasuries and corporate bonds. In particular, I want to hold blue-chip stocks with strong international and emerging market operations - I want to be on the right side of an inevitable long-term depreciation of the US dollar against emerging market currencies. While there will certainly be ups and downs, the relative wealth of the United States and Western Europe vs. the rest of the world will almost certainly decline over the long term. That being said, American companies are the best-run in the world, and a top-tier American company with substantial international operations trading at a reasonable multiple seems to me to be the ideal long-term investment.

As the market continues to rise, I’ve begun to look for potential shorts of overvalued and challenged businesses. I’ve also explored a number of other ways of hedging downside risk in a cost-effective manner. If the market continues to inflate, it is likely I add some short exposure in 2011.

Stock Holdings as of 12/31/2010:

During Q3 and Q4, I began shorting levered short ETFs (a short of a short) as a long term investment, including DPK (a 3x short of the developed market index EFA), SDS (the 2x short of the S&P500) and QID (a 2x short of the NASDAQ index). I also own put options on each underlying index as a hedge against short term declines. Due to a mathematical phenomenon known as the “constant leverage trap,” levered ETFs are a disaster as a long term investment (especially when volatility increases). This conceptually makes sense - a levered ETF is forced to re-balance daily in a manner designed to perform poorly over the long term. When its underlying investments increases in value, the ETF adds leverage, and when its underlying investments decrease in value, the ETF decreases leverage. At their core, levered ETFs buy high and sell low. The end result is that while levered ETFs do accomplish their intended mission (which is to replicate 2x or 3x the return or inverse return of an index daily), over a longer period of time, they are practically designed to do worse than their intended purpose. By shorting the levered short ETFs, I’m on the right side of the constant leverage trap, while utilizing zero-cost leverage on a long-term investment. These positions in the aggregate now make up the largest holding in the portfolio. Note that as a short, as the underlying indexes rise and the positions make money, the investment will actually decrease in value and importance (unless I decide to add to the position). During the quarter, I sold the stock holding in Raytheon for a small loss to free up cash for these positions.

Greenlight Capital Re Ltd. (GLRE), the Cayman Island reinsurance company founded by long-short hedge fund manager David Einhorn, continues to be a very large holding in the portfolio at roughly 30% as of year-end. As I’ve discussed in the past, the company has a number of advantages designed to result in very strong compound returns over many years - no corporate-level taxes, a superior investment manager, seasoned and prudent underwriters and a low cost structure. While my original purchases of the stock in 2008 and 2009 were at below tangible book value (net asset value), the stock now trades at 1.25x to 1.3x book value, which I believe is a reasonable price, while no longer a bargain. Nevertheless, I have no intention to sell this holding in the short term, as I believe the company has the potential to benefit from high returns on equity over many years. Einhorn’s investments had another strong year in 2010, earning 11% with a portfolio only modestly net long.

Goldman Sachs (GS) is the third largest holding in the portfolio through both a stock position, and an outstanding cash-secured put expiring January 2012. While GS has risen in recent weeks, it continues to trade at a single-digit earnings multiple and is well positioned to capture banking and trading fees and revenue as economic activity picks up. GS’s legal challenges are subsiding, and while GS’s incredible franchise took some populist hits after the banking crisis, its reputation within the business community is unbeatable (see the new Facebook private placement), and it continues to hire the best and the brightest on Wall Street. As I’ve noted before, I wouldn’t be surprised to see GS’ market share grow over the coming decade as its lesser competitors struggle through new financial regulations.

Through cash-secured puts, expiring Jan 2012 (MSFT) and Jan 2013 (CSCO), each at the $30 strike price, Microsoft and Cisco Systems represent the fourth and fifth biggest positions in the portfolio (in terms of risk). Each trades a a low-teens earnings multiple (before taking into account massive cash balances), generates incredible free cash flow and is well positioned to benefit from a global boom in technology spending. In early November, CSCO’s stock stumbled from the mid $20s to the high teens after John Chambers delivered a disappointing outlook on a conference call. I believe the market largely overreacted, focusing (as the market often does) too much on short term factors, and ignoring the long term strength of the CSCO franchise, its free cash flow generation, and its valuation. Note that CSCO is also purchasing an enormous amount of its shares, one reason I like the risk-profile of the cash secured put.

Medical device maker Becton Dickinson & Co. (BDX) is the fifth largest holding in the portfolio. BDX’s stock price has drifted upwards along with the market, but continues to trade at a reasonable earnings multiple. As discussed in past posts, BDX has an entrenched franchise, a strong international business (roughly 60% of revs come from outside the U.S.), and generates high returns on equity utilizing limited debt. As discussed above, BDX is the sort of blue-chip, well run business with international operations that makes for a compelling long term investment. As long as BDX’s earnings multiple stays within a reasonable range, I do not anticipate selling any time soon.

Offshore driller Noble Corp (NE) is the sixth largest holding in the portfolio. NE’s stock declined in April and May in connection with the BP Deewater Horizon incident. Given that the company had no involvement with the incident, and that only a modest percentage of its business came from US waters (a little over 20%), the sell-off appeared to be a market overreaction. Notwithstanding an over 30% increase in price since my original purchase, the stock still trades at a single-digit earnings multiple. Oil prices have risen substantially as economic activity has increased, and it appears that we’re unlikely to reduce offshore drilling over the next several decades. Following the Deepwater Horizon incident, NE management also completed an opportunistic acquisition of a competitor, Frontier Drilling, at a depressed price utilizing its large cash balance. Given NE’s low earnings multiple, conservative capitalization, opportunistic management, and the prospect of increasing energy costs, I continue to like NE as a medium to long term holding.

The remainder of the portfolio is made up modest stock holdings of three very strong international businesses, Yum Brands, IBM and Vodafone, which I continue to like over the medium to long-term based on their cash flow generation and valuations. The Q2 2010 summary includes longer descriptions of these holdings.

Sunday, January 9, 2011

Saturday, August 7, 2010

Kimberly-Clark Corporation Diagonal Call Spread (Update)

This last week, I closed out the Kimberly-Clark Corporation (KMB) diagonal call spread I opened in March of this year for a net profit of $759.17, and an IRR of 217%. I opened the position when KMB was trading around $62.50, and felt that its high dividend yield (4%), low earnings multiple and stable business (bathroom products) would provide a floor under the stock price. I also didn't feel that the stock had the potential to appreciate a great deal in the short term or "pop", and so chose to purchase a diagonal spread that would profit from time decay. As KMB stayed flat for several months, I was able to roll the short month option over twice. While I continue to feel that Kimberly-Clark offers solid value at today's prices, I've decided to lock in profit given the stock's recent rise. I'll monitor KMB and in the event of price weakness may enter into a similar position.

Friday, July 16, 2010

The Goldman Sachs Group, Inc. Put Sale

Today, I sold a Jan 2012 $170 put on GS for $3,970.48 in premium (including commissions), which adds to my current long position in GS stock. The break-even point of the put sale come Jan 2012 expiration is roughly $130, and the max-profit point is $170. Assuming the put finishes out of the money, I will have generated a real return on the cash required for exercise of approximately 30% over about a year and a half. If GS stays flat and finishes at $147.50 at Jan 2012 option expiration, the put would be exercised and I'd have generated a return of around 13% on the cash required for exercise.

Yesterday, GS announced a settlement of their SEC fraud suit in connection with their role in the synthetic collateralized debt obligation hand crafted by credit default buyer and hedge fund manager John Paulson. The settlement removes much of the uncertainty surrounding GS's future. While the ultimate impact of the financial regulatory reform bill is yet to be seen, GS's current price reflects a very pessimistic forecast for the company's profit potential over the coming years. With the SEC suit out of the way and many of GS competitors hampered if not gone forever, I think GS at today's prices will outperform the market over the coming years.

By selling a long term in-the-money put I am utilizing leverage, but it's an amount of leverage I'm comfortable maintaining given the cash portion of my portfolio (and the fact that I continue to deposit additional cash into the account). When using options, I look for opportunities to capitalize on non-recourse leverage, zero (or profitable, negative cost leverage) and sometimes both. A long term naked put sale is certainly recourse leverage so should be entered into with caution, but can offer an opportunistic investor a chance to benefit from zero-cost or in this case, profitable, negative cost, leverage through time decay. Note that with this put sale, GS can now be considered the second largest position in the portfolio.

Yesterday, GS announced a settlement of their SEC fraud suit in connection with their role in the synthetic collateralized debt obligation hand crafted by credit default buyer and hedge fund manager John Paulson. The settlement removes much of the uncertainty surrounding GS's future. While the ultimate impact of the financial regulatory reform bill is yet to be seen, GS's current price reflects a very pessimistic forecast for the company's profit potential over the coming years. With the SEC suit out of the way and many of GS competitors hampered if not gone forever, I think GS at today's prices will outperform the market over the coming years.

By selling a long term in-the-money put I am utilizing leverage, but it's an amount of leverage I'm comfortable maintaining given the cash portion of my portfolio (and the fact that I continue to deposit additional cash into the account). When using options, I look for opportunities to capitalize on non-recourse leverage, zero (or profitable, negative cost leverage) and sometimes both. A long term naked put sale is certainly recourse leverage so should be entered into with caution, but can offer an opportunistic investor a chance to benefit from zero-cost or in this case, profitable, negative cost, leverage through time decay. Note that with this put sale, GS can now be considered the second largest position in the portfolio.

Phillip Morris International, Inc. Diagonal Call Spread Update

Yesterday I closed out my diagonal call spread on PM for a very modest profit of $351.99, a 13% return on my capital at risk, and an IRR of 583%.

In hindsight, I should have allowed for more upside, and used a ratio spread where I bought more long term calls than I sold (similar to my WMT and KMB spreads). PM had declined substantially to around $46, a price I thought was unreasonably low. Ultimately, given the negative market sentiment when I opened the position I chose to protect my downside more and hope for a flat market. PM instead rose to the high $49s in a short time period. I'll continue to monitor the stock and look to enter into a similar position in the event of market weakness.

In hindsight, I should have allowed for more upside, and used a ratio spread where I bought more long term calls than I sold (similar to my WMT and KMB spreads). PM had declined substantially to around $46, a price I thought was unreasonably low. Ultimately, given the negative market sentiment when I opened the position I chose to protect my downside more and hope for a flat market. PM instead rose to the high $49s in a short time period. I'll continue to monitor the stock and look to enter into a similar position in the event of market weakness.

Wednesday, July 14, 2010

Q2 2010 Portfolio Summary

Each quarter, I will be writing a brief summary “letter” summarizing the performance of the WCC portfolio during the preceding quarter, as well as describing each of portfolio’s then-current holdings. I’ll also provide some very general market commentary but will not prognosticate about short term price movements, as I believe they are by and large completely random. This is the first of the quarterly “letters”.

Market Thoughts and Portfolio Performance:

During Q2 2010, the WCC portfolio returned -5.38% compared to -11.86% for the S&P500. For the first half of 2010, the WCC portfolio returned 13.52% compared to -7.57% for the S&P500, for a difference of 21.09%.

Since inception (1/22/2008) the WCC portfolio has returned 70.32% compared to -21.36% for the S&P500.

Note that the above return figures are the portfolio’s time weighted return compounded quarterly. This method strips out the distorting effects of cash deposits and withdrawals to create a useful comparison to indices or other money managers.

The second quarter of 2010 was extremely volatile as global macro concerns really dominated the discussion. We began the quarter with general optimism about an economic recovery, consumer spending and job creation, and ended the quarter far more pessimistic about the economy’s recovery (or the chance of a double dip recession), sovereign debt levels, sovereign debt defaults and the accompanying calls for fiscal austerity measures. I feel far more comfortable holding long term positions. During the quarter, we saw the prices of many cash rich blue chip American companies once again enter bargain territory - at quarter end Microsoft now trades at less than 10x, and Wal-Mart less than 11.5x forward earnings. Healthy small cap companies were driven to even lower multiples. For as much talk as there is about general market over-valuation, American blue chips are pricing in almost nonexistent growth over the coming ten years (inflation level EPS growth for Microsoft and Wal-Mart should result in solid returns over the coming decade at today’s levels). The market also appears to be ignoring the beneficial effect of recessionary cost cutting measures at market leading companies. The best American companies have been able to increase their bottom line without expanding the top line and as a result, bottom line growth should accelerate as we exit the recession and top line growth resumes. In sum, I think a buyer of blue-chip American companies at today’s levels should be rewarded over the coming decade

Stock Holdings as of 6/30/2010:

Greenlight Capital Re Ltd.: By a wide margin, the largest holding in the WCC portfolio at 39% is Greenlight Capital Re Ltd. (GLRE), the Cayman Island reinsurance company founded by hedge fund manager David Einhorn. As you can see, I don’t shy away from concentrated holdings but instead prefer them (its hard enough to find one good idea let alone many). The company writes reinsurance policies to various primary insurers and invests its float in Einhorn’s hedge fund Greenlight Capital. The company has the potential to be a compound return machine, benefiting from profitable underwriting (thus far), superior investment management thanks to Einhorn and his team, and no corporate level taxes. I began buying GLRE when it was trading in the $11s during the market crash, a price below its tangible book value. This bargain price didn’t last long and the stock now trades at a healthy premium to book and in the $26 range (the company’s investments through Greenlight Capital also performed well in the interim, increasing tangible book value substantially). While I am not purchasing additional shares at these price levels, I don’t intend to sell the stock and will hold until I believe it trades at an unsustainable multiple of tangible book. I hope this is in the distant future after GLRE is able to compound returns for a number of years. As I continue to deposit cash, GLRE’s weighting in the portfolio will decrease. Note that Einhorn has maintained a healthy level of skepticism about the equity markets and a large short portfolio. GLRE’s investment portfolio is up .6% on the year vs. a down market.

Goldman Sachs Group Inc.: At roughly 7.5%, Goldman Sachs Group Inc. (GS) is the second largest holding in the portfolio. I bought GS two times during the quarter in the mid $140s after the announcement of the SEC’s fraud case against the investment bank. GS now trades at slightly over its tangible book value and at a mid single digit trailing earnings multiple. I think it likely that the SEC’s case against the firm will result in a financial settlement which doesn’t damage the going concern value of the firm. I also think that the market’s pessimism surrounding the financial reform bill is over blown and the large investment banks will continue to be extremely profitable enterprises over the coming decade. I’d also note that one side effect of intense regulation in an industry is a weakening of smaller players with fewer resources, while strengthening and further entrenching the larger players (see Phillip Morris in the era of intense tobacco regulation). I wouldn’t be surprised to see GS’ market share grow over the coming decade as its lesser competitors struggle in heavy regulatory environment.

Becton Dickinson & Co.: At roughly 7%, the entrenched medical supply maker Becton Dickinson & Co. (BDX) is the third largest holding in the portfolio. BDX is an incredibly efficient company with an enviable market position and growth record which trades at very modest multiples due to concerns about the new health care regulations. BDX now trades at around 12x forward earnings and 7.5x EV/EBITDA despite a 10 year EPS growth rate of almost 17%. It maintains very high returns on assets in the mid teens and returns on equity in the low to mid 20s despite the use of little debt. Note that BDX is also a holding of Warren Buffett as well as David Einhorn’s Greenlight Capital. Often one’s best ideas are borrowed. I originally entered my position in BDX by selling long term put options. Following the recent market decline, I took a realized loss on the put option by repurchasing it (which should help come tax season) and purchased the stock outright. I may look to sell additional long term put options at some point in the near future.

Noble Corp: The offshore oil driller Noble Corp (NE) is the portfolio’s fourth largest holding at 6.4%. Following BP’s Deepwater Horizon disaster and the Obama administration’s moratorium on deepwater drilling, shares in the offshore drilling companies plummeted to mid single digit earnings multiples. NE is the second largest driller in the world after Transocean, and has a long term and very profitable relationship with Royal Dutch Shell. The company recently announced several new contracts with Shell as well as the opportunistic purchase of smaller competitor Frontier Drilling in a cash transaction. NE maintains a healthy balance sheet and is able to fund the Frontier acquisition with cash on hand and borrowings under its existing credit facility. While the drilling moratorium will certainly hurt NE’s earnings this year, only around 22% of the company’s revenues come from US waters so the company will maintain solid profitability. Long term, I think we may have no other choice but to continue our offshore drilling to meet our energy needs.

Yum Brands Inc.: At 6%, Yum Brands Inc. (YUM), the operator of Taco Bell, Pizza Hut, KFC and lesser known restaurants A&W and Long John Silver’s, is the fifth largest holding in the WCC portfolio. YUM is an incredibly successful business that generates terrific returns on assets in the mid teens and is growing at a brisk pace, particularly internationally where its brands (KFC in particular) arguably have more appeal than they do in the US. There are roughly 3x the number of KFC’s in China than McDonald’s. YUM is the sort of business I get very excited about. It’s capital light, simple, has sustainable brand appeal and terrific international growth opportunities. It’s certainly not the cheapest stock in the portfolio, at around 15x forward earnings or 18x trailing earnings, but I believe it remains undervalued given its potential for growing cash flow generation and scale.

International Business Machines Corp.: At 5.13% of the WCC portfolio, IBM is the sixth largest holding. This massive tech mainstay is firmly entrenched and has unmatched scale in delivering enterprise software and hardware solutions to the world’s companies and governments. While trading near an all time high price, it trades at a 10 year low multiple of earnings (around 10.5x forward earnings). CEO Samuel Palmisano has delivered and is currently delivering on his strategy of selling off commodity hardware business and developing high end and stickier software and services businesses. The company spits off an incredible amount of free cash flow which management has historically used both for massive stock repurchases and acquisitions. Mr. Palmisano has recently announced he expects the company to double EPS over the next five years. Note that while my stock holdings of IBM only represent roughly 5% of the portfolio, I’ve also sold a long term put on IBM expiring in October, effectively increasing the portfolio’s allocation to IBM.

Vodafone Group Plc: At around 4.8%, Vodafone Group Plc (VOD) is the smallest stock holding in the WCC portfolio. VOD is an enormous international mobile telecommunications network provider with dominant market positions in Europe, a large presence in India and Asia and the US with 45% of Verizon Wireless, a joint venture with Verizon Communications, Inc. The stock is cheap (trading at less than 10x earnings and an even more favorable price/free cash flow ratio), and even cheaper if one takes into account the unrealized earnings from its ownership of Verizon Wireless. (Under accounting rules, VOD doesn’t account for its share of Verizon Wireless’ earnings on its own income statement, but rather just any dividends paid by Verizon Wireless to VOD. Verizon Wireless doesn’t pay dividends to its parent companies now, but will likely begin paying dividends soon as it has or is near paying off inter-company debt to Verizon Communications, Inc.) As VOD pays over a 7% sustainable dividend, I am comfortable holding VOD and waiting for cash flow growth and/or multiple expansion.

Option Positions as of 6/30/2010:

In addition to the IBM put I’ve sold which I reference above, several diagonal call positions make up the remainder of the WCC portfolio. These positions, on Wal-Mart Stores, Inc. (WMT), Microsoft Corporation (MSFT), Phillip Morris International, Inc. (PM) and Kimberly Clark Corporation (KMB) are designed to generate return similar to a covered call, benefiting from a flat to slightly up market, but benefiting from the use of non-recourse leverage. These positions have been generally flat through a down market in Q2 2010.

Thursday, July 1, 2010

Rick's Cabaret International, Inc. Put Sale

Today I sold seven August 2010 $7.5 puts on strip club operator Rick's Cabaret International, Inc. (ticker: RICK) for aggregate proceeds of $547.54. If the puts are in-the-money at August expiration, I will allow them to be exercised and will purchase the stock. If the puts expire worthless, I will have generated a 10.4% return on the reserved cash required to exercise the puts over a period of roughly a month and a half ($547.54 premium divided by $5,250 in reserved cash).

I've had a position in Rick's before, buying the stock in the $5s and down into the $3s during the height of the 2008 market crash. I then sold the stock for roughly $15.50 in March of this year (my sale price was effectively less because of covered calls I had sold against my position). The stock has since dealt with a failed acquisition of VCG Holding Corp., the only other publicly traded strip club operator, and the general market decline and the stock is back down to the mid $7s. At current prices, the stock trades at less than 10x trailing earnings (about 6-7x forward earnings) and the company has seen a considerable uptick in business over the last six months. The company generates solid cash flow (free cash flow is greater than net income due to large depreciation deductions) which it uses for other strip club acquisitions. At its core, RICK is a consolidation play, and RICK is able to purchase locally owned "mom and pop" strip clubs at very low multiples (3-4X EBITDA).

I've had a position in Rick's before, buying the stock in the $5s and down into the $3s during the height of the 2008 market crash. I then sold the stock for roughly $15.50 in March of this year (my sale price was effectively less because of covered calls I had sold against my position). The stock has since dealt with a failed acquisition of VCG Holding Corp., the only other publicly traded strip club operator, and the general market decline and the stock is back down to the mid $7s. At current prices, the stock trades at less than 10x trailing earnings (about 6-7x forward earnings) and the company has seen a considerable uptick in business over the last six months. The company generates solid cash flow (free cash flow is greater than net income due to large depreciation deductions) which it uses for other strip club acquisitions. At its core, RICK is a consolidation play, and RICK is able to purchase locally owned "mom and pop" strip clubs at very low multiples (3-4X EBITDA).

Sunday, June 27, 2010

Phillip Morris International, Inc. Diagonal Call Spread

I've long wanted to open a position in Phillip Morris International, Inc. (ticker symbol: PM). It's an incredibly robust business with about as sticky a consumer product as is possible. Unlike its domestic cousin Altria Group, Inc. (ticker symbol: MO), PM also operates in a number of international jurisdictions with far less onerous regulations, taxes and other anti-smoking governmental programs (amoral as that sounds). Furthermore, declining smoking rates in Western Europe have been offset by increases in various emerging markets. PM produces an incredible amount of free cash flow available for stock buy backs and dividends, and operates with extremely high returns on assets (in the low 20s). Following a large price decline, the stock now trades at just over 13x last year's earnings and it supports a very sustainable 5% dividend.

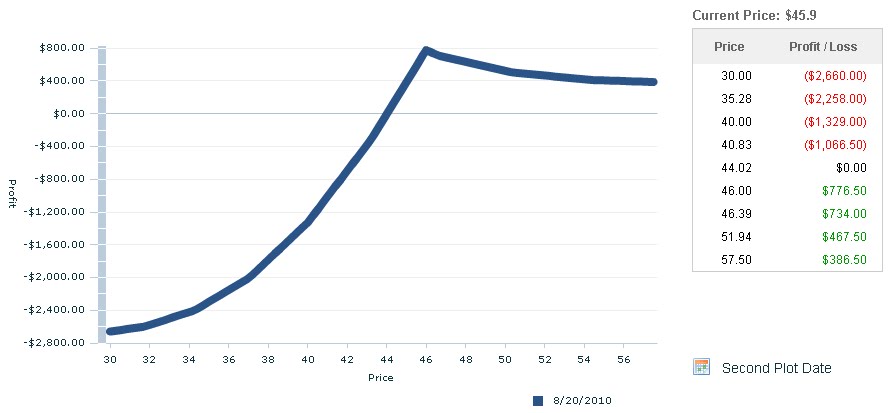

To gain leverage while capturing time decay, last Tuesday I purchased 5 diagonal call spreads on PM, purchasing the Jan 2011 40s, and selling the August 2010 46s, for a net debit of $2,733.97 including commissions. This spread will prove solidly profitable if the stock stays around the $46 range through August expiration, and modestly profitable above $46. (See the profit/loss chart below for a graphical description of this position. Note, however that OptionsXpress tends to inflate the implied volatility of the long-side of the spread at expiration so the actual profit potential could be less than the chart shows if volatility were to decline). This sort of diagonal call spread has the characteristics of a levered covered call and can be an appropriate source of leverage where the underlying stock has considerable price support.

If the stock does stay below $46 at the August expiration, I'll look to purchase the August calls back and sell later month against the Jan 2011s.

To gain leverage while capturing time decay, last Tuesday I purchased 5 diagonal call spreads on PM, purchasing the Jan 2011 40s, and selling the August 2010 46s, for a net debit of $2,733.97 including commissions. This spread will prove solidly profitable if the stock stays around the $46 range through August expiration, and modestly profitable above $46. (See the profit/loss chart below for a graphical description of this position. Note, however that OptionsXpress tends to inflate the implied volatility of the long-side of the spread at expiration so the actual profit potential could be less than the chart shows if volatility were to decline). This sort of diagonal call spread has the characteristics of a levered covered call and can be an appropriate source of leverage where the underlying stock has considerable price support.

If the stock does stay below $46 at the August expiration, I'll look to purchase the August calls back and sell later month against the Jan 2011s.

Subscribe to:

Comments (Atom)